Introduction:

Weather/climate is to farming, as commerce/economics is to business.

The field of Economics teaches you where the economic and material dominoes fall and how to think in broader models with lesser or greater precision depending on your analytical needs. Additionally, studying economics humbles you about the complexity of our society, and helps you understand what question(s) you have a higher or lower probability of being able to answer.

In this blog post I am going to attempt to convey to the reader the most important concepts and insights I learned while pursuing an economics degree. We will keep our scope strictly to economics rather than also covering the typical general education covered in a 4 year degree.

This blog post will be my perceptions and what I learned from my perspective. There are plenty of articles covering the standard economic concepts so we will not be covering those in depth, only as reference. We will be diving deeper and looking with a more discerning eye to determine what the key takeaways are from studying the subject and how these takeaways can structure your thinking.

I will try to talk about the counterintuitive aspects, the hidden aspects, instead of the models you all know. Obviously I cannot synthesize all I learned in 4 years, but I am going to try to synthesize what I found most valuable.

In some ways, I am writing this post just to strengthen my own understanding of the subject.

Disclaimer:

I would like to express humility and caution to the reader as to the fact that I am not a PhD. If you are a practitioner in the field and you see any errors please comment. If you are someone who has studied these things deeply you may also comment on my interpretation.

Remember this disclaimer if you disagree with something. It is okay to disagree.

Due to the length of this post here is a table of contents:

Table of Contents:

Classical & Neoclassical Economics - The Beginning of Measurement

Behavioral Economics - Promise, Observation, & Measurement Issues

Limits, Errors, Omissions, Gaps, & Lags (This is the best section)

The (Evolving) Definition & Scope of Economics

Economics has been defined in many ways:

1. Classical Definition: Economics is the study of how societies allocate scarce resources to satisfy unlimited wants and needs.

2. Lionel Robbins's Definition: Economics is the science which studies human behavior as a relationship between ends and scarce means which have alternative uses.

3. Paul Samuelson's Definition: Economics is the study of how people and society end up choosing, with or without the use of money, to employ scarce productive resources that could have alternative uses, to produce various commodities and distribute them for consumption, now or in the future, among various persons and groups in society.

4. Alfred Marshall's Definition: Economics is a study of mankind in the ordinary business of life; it examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requisites of wellbeing.

5. Milton Friedman's Definition: Economics is a science which studies human behavior as a relationship between ends and scarce means that have alternative uses.

6. Jacob Viner's Definition: Economics is what economists do.

7. John Maynard Keynes's Definition: Economics is a science of thinking in terms of models joined to the art of choosing models which are relevant to the contemporary world.

8. Gary Becker's Definition: Economics is the systematic study of the production, distribution, and consumption of goods and services.

9. Joan Robinson's Definition: Economics is a study of the ways in which people earn their living.

10. John Stuart Mill's Definition: The science which traces the laws of such of the phenomena of society as arise from the combined operations of mankind for the production of wealth, in so far as those phenomena are not modified by the pursuit of any other object.

In summary; Economics consists of the study of our material reality, and how we sustain ourselves, both individually and collectively. It studies how people, organizations, and societies decide what to do with limited resources to achieve their intentions and what is more or less effective in doing so.

Those definitions all provide valuable perspectives and insights on the evolution of the definition. However, I think the definition is simpler. In many ways economics can be termed as the study of the human organisms quest for survival, growth, prosperity, and reproduction.

The classical definition of economics isn't broad enough. Economics is about life. So far in the field we have measured everything in money, or other monetarily derived measurement systems like GDP, GNP, Productivity, etc. The imposition of alien measurement systems onto everyday life has caused many perversions of thought. Economics had typically excluded unpaid work such as housework, childcare, charitable work, volunteering, and more — simply because it couldn’t be measured in monetary terms. These human behaviors are clearly economically valuable actions/work. Any work that pertains to survival, growth, betterment of life, and reproduction, is economic in my mind.

Government and religion have typically been excluded from the definition and scope of Economics and I disagree with that. The Government is an economic industry that provides economic services such as governance, infrastructure, justice, defense, and more. Religion is an economic industry that provides peace of mind, faith, resilience, and community support.

There has been a yearning by economists to abstract economics from politics, and there has been some fruit to that process, but in reality, the laws of a nation are another input into the system of the economy and therefore economics is difficult to study without incorporating the paradigm of politics. No matter how much you wish to separate the two, they are inseparable. Those who study Political Economy have discerned that.

Political economy is a broader term that incorporates economic analysis but also considers the relationship between economics and political institutions, power structures, and social systems. Political economy examines not only the economic aspects but also the political and social dimensions of decision-making. It is concerned with issues of power, distribution, and the impact of political structures on economic outcomes.

The definition of Economics must be broad and we must consistently give research freedom to our academic practitioners as they explore new concepts, angles and perspectives in the quest for truth, knowledge, or enlightened perspective. As for private sector economists, their job is primarily to provide numerical assessments for institutions to make decisions from. There is the old management maxim that if it can’t be measured it can’t be managed. There is some truth to that. Though you will be hard pressed to find a private sector economist who does not have to integrate the affects of upcoming legislation into their models, so their definition has already broadened, and any economist hoping to understand the labor market will inevitably have to dive into culture, beliefs, and the changing generational paradigms to better understand the market’s ebbs and flows.

In summary, the broader the definition of economics the better. No doubt practitioners in academics and the private sector will have to narrow their scope for their own productivity, but the discipline itself, lest we risk in the box thinking, must be defined as broadly as possible. Therefore, my definition of economics is the study of the human organisms quest for survival, growth, prosperity, and reproduction. In this light, the field would be considered a subset of biology; indeed ants and bees have primitive economies that exhibit infrastructure and division of labor. Economics in its very essence is about how organisms survive and thrive.

With the scope of our topic covered, let's move on to its nature.

The Economy as a System

The emergence of Systems Science has given us great insight into the behavior, dynamics, and properties of complex systems. Early in the development of Economics, the scientific zeitgeist of the time was inspired from the perspective of the “Mechanical Universe” popularized by the burgeoning success of physicists at the time. Economists boldly anticipated that they would be able to predict economic behavior and the behavior of the economy as a whole with the same predictive accuracy as Newton’s laws of motion:

"The ultimate aim of political economy is to reduce it to an exact science, and to bring it within the domain of mathematical reasoning." - William Stanley Jevons (1835-1882)

"Just as mechanics explains the equilibrium of physical forces, so political economy explains the equilibrium of social forces." -Leon Walras (1834-1910)

Jevons, a key figure in marginalism, believed that economics could be reduced to a set of mathematical laws similar to physics. This assumption is forgivable as it was made during a time ignorant of emergent properties, complexity theory, and chaos theory. Thankfully, systems science came to the rescue.

(As a bonus, here is a decent mechanistic overview of the economy that does have utility: How The Economic Machine Works by Ray Dalio)

The Economy is a Complex Adaptive System

“A complex adaptive system (CAS) is a dynamic and interconnected network comprised of diverse and autonomous or [semi-autonomous] agents or components that continuously interact with each other and their environment. These systems exhibit emergent behavior, where collective patterns and properties arise from the local interactions of individual elements, often leading to non-linear and unpredictable outcomes. CAS possess the ability to self-organize, adapt, and evolve over time in response to changes or perturbations, allowing them to exhibit resilience and flexibility. The behavior of a complex adaptive system is shaped by feedback loops, where the consequences of actions influence subsequent behaviors, contributing to the system's capacity for learning and adaptation. Examples of CAS range from ecosystems and economies to social networks and biological organisms, reflecting the ubiquitous nature of these intricately structured systems in various domains.” - ChatGPT

Understanding that the economy is a CAS is crucial for anyone pursuing the subject. We all wish there were easy linear relationships in most of life, but even if you can mathematically illustrate an economic relation linearly, it does not mean it is linear in actuality. It only means you abstracted the relation to a degree that it appears linear (though your linear abstraction may have utility). The economy is too complex for that, and this is where one of the crucial aspects of studying economics comes in: humility.

Recognizing the economy as a complex adaptive system (CAS) has profound implications for the field of economics. Unlike the early aspirations of predicting economic behavior with precision, understanding the economy as a CAS acknowledges its inherent complexity, non-linearity, and unpredictability. In a CAS, emergent properties arise from the intricate interactions of diverse agents and components, leading to dynamic and often unpredictable outcomes. This complexity introduces a level of uncertainty and limits the extent to which economic phenomena can be accurately described or predicted.

The presence of feedback loops further complicates matters, as the consequences of actions in the system influence subsequent behaviors, creating a continuous cycle of adaptation and evolution. This reality calls for a more humble approach in the pursuit of economic knowledge, emphasizing the importance of acknowledging the inherent uncertainties and limitations in predicting economic dynamics. In essence, the economy's nature as a CAS challenges economists to embrace a more flexible and adaptive mindset, understanding that predicting every facet of economic behavior may be an elusive goal due to the system's inherent complexity.

Not only that, the inputs to the economic system include elements that are not typically considered economic. Philosophy(ies), belief systems, zeitgeists, cultures, personalities, geopolitics, attitudes and more affect economics like a reflexive strange loop and are nearly impossible to quantify and measure objectively.

We may wish inputs were linear but they really act like a reflexive strange loop where the outputs themselves are inputs in a forever recursive and evolving process that is both robust and delicate. There are no exogenous variables. Treating something as exogenous should only be done to gain greater clarity on an underlying variable. The culture of a nation, the philosophical zeitgeist, and the prevailing paradigm manifest in belief systems that form the core of economic reality during any given time. As these change so to will the economy.

In fact, there is nothing exogenous to the economy. Even leisure time serves the utility of restoring the worker for another day of productivity. Geography sets the economy’s precedent, philosophy sets the beliefs, STEM sets its material capabilities, psychology forms its behavioral troughs and riverbeds, etc. All of a human life, in its entirety, structures how humans make decisions about resources and life.

This makes economics a difficult field to study.

It means our economic predictions have some upper limits on precision and relative probability assignment. However, with great effort, some progress can be made in the field of economics and our understanding of the economic world. These systems do have rhythms and pulses (typically called cycles) that can be discerned over time and with appropriate data analysis assuming you have accurate and timely data.

Therefore, I have learned it is best to pursue economics with systems thinking, flexible axioms, adaptive methods, a skeptical eye towards the reliability of data, and most importantly, humility.

(What’s really trippy is when you find out the field of economics itself is a CAS)

With the nature of our topic covered, let's move on to its foundations.

Classical & Neoclassical Economics - The Beginning of Measurement

Neoclassical Economics (NE), is my favorite abstract delusion. As a management suggestion NE has utility, as a predictive framework it is like playing with expired dynamite.

Neoclassical economics is a school of economic thought that emerged in the late 19th century, building upon classical economics and aiming to provide a more systematic and mathematically rigorous framework for understanding economic behavior. Neoclassical economists emphasize the role of individuals and organizations as rational decision-makers who seek to maximize their utility (satisfaction) or profit, subject to various constraints such as budget limitations.

For purposes of clarity we are going to further define it as the set of base economic models the field uses, the belief in rational behavior, the belief in market efficiency, broadly the Chicago School of Economics, and all those who really think we can quantify everything.

I would describe neoclassical economics as ‘economic behavior in a vacuum’ (ceteris paribus - “with other conditions remaining the same” is the typical way this is expressed). NE models would be correct if you isolated every other variable, stripped the CAS that is the economy down to its basic parts, and simplified it into a 1970s computer game.

Lets Explore the subject further.

Homoeconomicus (Rational Decision Makers)

At the foundation of NE is the assumption/central axiom of “homoeconomicus” or “Economic man”. It is the characterization of the human or organization as a rational agent who seeks to maximize their own personal wealth or utility for the express purpose of self-interest. It does not clearly define what “utility” is for the individual but it clearly defines “utility” for firms as profit maximization.

It assumes the following about individuals and organizations:

Rationality: Individuals are rational actors who make decisions by systematically working through all available information and options to maximize their utility or satisfaction. This implies that people are capable of ranking their preferences in a coherent and consistent manner.

Self-Interest: Each individual acts in their own self-interest, seeking to maximize their own welfare, utility, or profit. This does not necessarily mean that individuals are selfish in a moral sense, but rather that they prioritize their own outcomes in decision-making.

Complete Information: It is assumed that individuals have access to all the information they need to make their decisions, including knowledge of all the available options and the potential outcomes of each choice. In reality, this assumption is often relaxed to allow for information asymmetry and imperfect information.

Utility Maximization: Choices are made based on the goal of utility maximization. For consumers, this means selecting goods and services that provide the highest level of satisfaction. For producers, it involves choosing production methods and outputs that maximize profits.

Marginal Decision Making: Economic actors make decisions at the margin, meaning they evaluate the additional costs and benefits of changing their current state by a small amount. Decisions are made based on marginal analysis (weighing marginal benefits against marginal costs).

Consistent Preferences: Individuals have stable and consistent preferences over time. Their choices reflect a coherent and consistent ordering of these preferences.

No Influence of Emotions: Decisions are not influenced by emotions; they are made purely on the basis of rational calculations. Emotional factors and psychological biases are assumed to be irrelevant in the decision-making process.

Unlimited Cognitive Ability: Homo economicus is presumed to have unlimited cognitive abilities to process and evaluate information. This assumption underpins the ability to make rational decisions based on complex information.

In the realm of scientific axioms, this is one of those rare assumptions/axioms that can be disproven from anecdotal evidence alone. Our lives are littered with examples both from ourselves and from others that disprove all or most of the above assumptions and proliferate enough to qualify for the statistical rule of large numbers. No one (or even organization) makes decisions with purely neoclassical frameworks except psychopaths, and even they don’t have the processing power necessary to optimize the decision of where to buy gasoline in a medium sized city.

But the concept/axiom/assumption of “homoeconomicus” does serve its purpose, it provides us a beginning framework for thought, observation, and measurement. We make the previous assumptions, create an objective function (based on utility maximization), and build models around it about what type of decisions economic agents would make given a set of options in order to maximize their utility.

When the models are complete, we superpose them onto reality, make predictions, record data, then the differences between our theory and observations will slowly get us closer to truth.

It is a useful beginning in the exploration of individual or organizational economic behavior, but the idea it represents behavior accurately is irrational and disproven both anecdotally and academically.

NE Microeconomic Models

Microeconomics focuses on the actions of individuals and industries, like the dynamics of supply and demand for goods and services, and the behavior of individual markets and market structures (e.g., perfect competition, monopoly, oligopoly, and monopolistic competition).

Within the NE framework, several base microeconomic models are commonly used:

The Supply and Demand Model: This foundational model describes how the price and quantity of a good or service is determined in a market. It posits that in a competitive market, the unit price for a particular good will vary until it settles at a point where the quantity demanded will equal the quantity supplied, resulting in an economic equilibrium for price and quantity transacted.

The Theory of Consumer Choice: This model explores how consumers maximize their utility (satisfaction or pleasure) given their budget constraints. The theory uses the concepts of indifference curves and budget constraints to explain consumer choices among various goods and services.

The Production Theory: This model looks at how firms aim to maximize profits by deciding how much to produce and at what cost. It examines the inputs (labor, capital, etc.) used in the production process and how changes in these inputs affect the output of goods and services.

Various Market Models: Microeconomic models that describe the structure of different types of markets such as The Perfect Competition Model, The Monopoly Model, The Oligopoly Model, The Monopolistic Competition Model.

The General Equilibrium Theory: This advanced model looks at how supply and demand in multiple markets interact and come to an equilibrium. It extends the analysis of equilibrium from one market to the economy as a whole. This is a more complex case. While it has microeconomic foundations—concerning itself with the interaction of supply and demand across multiple markets—it can be extended to macroeconomic applications through its analysis of the overall economy's resource allocation and the interactions between different sectors. Therefore, general equilibrium theory bridges microeconomics and macroeconomics, serving as a fundamental link between individual market analyses and aggregate economic phenomena.

Markets have fundamental forces that pull them to trend to equilibriums but are too volatile to ever be in an equilibrium state. Markets are in a continuous state of exogenous shocks, big and small. Market equilibrium should be considered a fundamental force but something that never gets actualized.

NE Macroeconomic Models

Neoclassical economics extends its principles to macroeconomics, focusing on the aggregate behavior of economies. The standard base macroeconomic models of neoclassical economics aim to explain economic growth, fluctuations, and policies using assumptions of rational behavior, market equilibrium, and efficient resource allocation. Here are some of the foundational models:

IS-LM, Mundell Fleming, The Solow-Swan Growth Model, The Ramsey-Cass-Koopmans (RCK) Model, The Overlapping Generations Model (OLG), The Real Business Cycle (RBC) Theory, The New Classical Macroeconomics Models, The New Keynesian Macroeconomics Models, The Dynamic Stochastic General Equilibrium (DSGE) Models.

These models are beyond the scope and intent of this blog post as I am trying to highlight a unique approach and overall framing of how one should (could?) approach economics. So I linked them and will let the curious reader explore them on their own.

Problems:

The problems with these macroeconomic models stem from the same problem with the neoclassical microeconomic models. NE base axioms/premises/assumptions are spurious at best if not outright wrong at worst. I also believe they don’t appropriately account for emergent factors. In NE the sum is 1+1=2 whereas in complex adaptive systems 1+1=3 as new dynamics emerge out of complex interactions.

With that being said, there is some utility to these models.

How to use them (what they are good for)

As you establish base premises (the beginnings of a model) you establish biases for future contradiction in all rational models, including the theoretical conceptual models above. The above models are idealized models on how economic behavior should occur. They do not represent reality. However, they have quite a bit of value as a starting point for economic analysis on the behavior of agents, industries, markets, and economies. Their value is as a starting point for measurement. Let’s walk through this.

Once a model is established, you impose or superimpose it onto reality.

Let us assume that the following image represents an economic model:

And let’s say, this is the actual underlying reality:

You superimpose your model on the reality, observe, start to measure against it:

The deviations from your model you discern, observe, and record are immediately noticeable and highlight areas for further investigation, deeper understanding, and model enhancement. Reality will almost always deviate from your model (unless you are about to win a Nobel Prize) and this means you have the opportunity to learn more. As you go through this iterative process your model should (hypothetically) get more accurate. This approach can be done in any domain whether you are modeling the economy, the price elasticity of demand for your new yoga pants line, or are trying to model the behavior of others. This process is domain agnostic.

Models are abstracted, they are not real, it’s like measuring a set of economic activity within a vacuum, but what that does provide you with is the ability to begin measurement, track deviations, and root out their cause. This is the basis for progress in most sciences.

There will always be better beliefs, better models, better knowledge. There is always something better to replace whatever you currently hold as true with. The litmus test is simply whether or not the model is predictively adequate for your purposes - whatever they may be.

Multi-Perspectival Approach:

In addition to imposing models onto reality, you need to be able to switch between models during the process of analysis. You need a collection of models that you understand with which you can switch between depending on the context and what the analytical situation demands.

Certain models work better for certain domains, phenomena, or instances. This is why you need to know many but not strictly adhere to any of them.

Have you ever been in an optometrists office (or seen this process via media) where the optometrist provides a series of different lenses and asks your if your vision becomes better or worse? This is the same process with the application of models. You have a collection of models (lenses), and given a particular analytical situation, you switch between them seeing which one provides further clarity and which one makes things fuzzier.

In psychology the Freudian models of the mind (id, ego, and super ego) have somewhat been discarded due to cognitive science, however, they still possess utility when discussing the mind. Economic models are similar. Go with the model that provides the most clarity for the situation.

Do not become addicted to one model. It is intellectual laziness.

In Management:

Neoclassical Economic Models such as those outlining maximization of productivity, output, profit, hiring, pricing, etc., all have decent utility as management suggestions. If you are able to explicate your operational processes into an objective function then these models do tell one how they could maximize these elements within their business and this is obviously valuable.

However, there are human costs with following neoclassical models in management. I consider these models management suggestions and not management maxims because you cannot run an organization without some economic waste which could very well be an investment in a person, place, or thing invisible to the balance sheet.

An organization or a business itself is a very human enterprise (at least in its current form) and there might be times when you focus on employee wellness instead of maximum productivity. In fact, a manager could find out they maximized productivity and eroded the intangible and invisible asset on their balance sheet called “employee good will”. At this point they would find out they maximized efficiency only for their company to become no longer effective. Over obsession with the financial performance of a company will dwindle your long term competitiveness.

Additionally, each industry has its own operating procedures and norms. In creative industries you wouldn’t push someone to the max thereby stunting the creative process, and in manufacturing pushing someone to the point of creating an accident is as dumb as it comes. You could end up with a disaster of such a magnitude that your company is ruined. You have to apply Wisdom in your application of neoclassical models for management and know when you have gone too far.

Economics is not so simple. Neoclassical microeconomic models are just management suggestions idealized. The over application of microeconomic models in an organization can result in the loss of the emergent qualities of camaraderie, solidarity, and community. Apply them at your own risk.

How Not To Use Them - Dangers & Hidden Costs

Neoclassical economic models, if over-applied and applied with hubris, can actually be extremely dangerous.

We have already covered that over adherence to these models within an organization can affect your long-term competitiveness, but when applied to the market as a whole to determine either policy or investment procedures, it can be disastrous.

The over adherence to these models led to the collapse of Long-Term Capital Management (LTCM) in 1998 that nearly bankrupted Wall Street and caused significant economic hardship.

Neoclassical Economics Conclusion - Proceed With Caution

There is some great irony in neoclassical economics. The field and models attempt to be so rational that they do the most irrational thing possible and describe the human economic agent as infinitely rational. Put another way; the field is obsessed with rationality while itself being irrational.

NE taken literally is a form of delusion. NE taken as a beginning framework for measurement and as a decent management suggestion is awesome.

Therefore, I describe neoclassical economics as a management suggestion and a measurement framework. If you take neoclassical economics outside these parameters it is a form of insanity as the data clearly indicates it is wrong.

When it comes to NE’s predictive and descriptive ability, it is limited to none. This is where Behavioral Economics attempts to take the torch.

Behavioral Economics - Promise, Observation, & Measurement Issues

From neoclassical economics, which is theoretical and made by a bunch of pseudo hyper-rationalists conceptualizing us all as economic automatons, we go to behavioral economics, which is more empirical but yet has some issues of its own.

Behavioral economics is a field of study that combines insights from psychology and economics to examine how individuals make decisions. It challenges the traditional economic assumption that individuals are rational actors who always make decisions in their best interest based on available information. Instead, behavioral economics acknowledges that various cognitive biases, emotions, and social factors can influence decision-making processes in ways that deviate from what classical economics would predict.

Empiricism plays a crucial role in behavioral economics by grounding theories and hypotheses in observable and measurable evidence. Unlike classical/NE economics, which often relies on theoretical models based on assumptions of rational behavior, behavioral economics emphasizes the importance of empirical data to understand how people actually make decisions in the real world. This approach allows for a more accurate and nuanced understanding of economic behavior that incorporates the complexities of human psychology.

With time, resources, and effort, Behavioral Economics has the ability to reform the base axioms of our economic models based on observation and not economic philosophy. It can replace the foundation of economics and provide us with a better model (or collective set of models) that replaces Homo Economicus to better describe how individuals and organizations make decisions. From there, we can rebuild our models into more accurate versions that hopefully have better descriptive and predictive abilities.

But behavioral economics faces its own set of challenges. Behavioral economists can collect data from laboratory experiments, field experiments, survey’s and questionnaires, observational studies, neuro-economic methods, big data, and machine learning. All of these have potential issues with the reliability of the data and the replicability of the results.

Furthermore, when observing humans, generations differ between one another; beliefs, culture, and trends change quickly, and you can never actually get inside peoples heads to know what they are truly thinking (unless Elon Musk’s Neuralink has more capabilities than we’ve been told!). All these problems affect the descriptive and predictive capabilities of the theories coming out of behavioral economics.

Behavioral economics will struggle to describe and model human behavior because it is simply too complex and the feedback loops that change human consciousness can upend the models they’ve had success with in only a matter of a decade or significant event.

For these reasons, the predictive value of behavioral economics will most likely be limited. But it is an extremely valuable and insightful field nonetheless.

Marxian Economics

Marxian Economics (ME) is simply too contentious and prevalent not to cover in this write up.

ME is a school of economic thought based on the work of the 19th-century economist and philosopher Karl Marx. It focuses on the critique of capitalism and the analysis of its economic processes. ME is distinguished by its attention to the historical and social context of economic activity and its emphasis on the conflict between different classes in society, particularly between the capitalists (those who own the means of production) and the workers (those who sell their labor).

Marx, ME, and how to engage with this subject, is quite misunderstood. Questioning capitalism has utility and a place within academia and intellectuals as we continue to evolve our ideas around what constitutes a well functioning economy. Though I disagree with ME’s foundational axiom (The Labor Theory of Value), there is some value to take away from ME, namely Marxian Method. Before diving into that, it is better if we cover the historical backdrop to better understand what conditions this school of economic thought was developed in.

Historical Backdrop

Marxian economics developed in the context of the rapid industrialization and economic changes occurring in Europe during the 19th century. While we have seen massive improvements in the quality of life from capitalism, we must remember, this time was notorious for its brutal working conditions such as:

Textile Mills Exploitation: In Britain, the cradle of the Industrial Revolution, textile mills were notorious for their harsh working conditions. Workers, including a significant number of women and children, worked up to 16 hours a day in poorly ventilated, overcrowded factories. They faced dangerous conditions, with frequent accidents, deaths, and occupational diseases being common. The wages were meager, and the employment of children allowed for even lower wage costs.

Coal Mining Conditions: Coal miners worked in extremely hazardous conditions, facing the constant risk of explosions, collapses, and coal dust inhalation. Child labor was rampant, with boys as young as five working as "trappers" to open and close ventilation doors. The long hours, lack of safety equipment, and minimal pay highlighted the severe exploitation of workers crucial for powering the industrial age.

The historical backdrop was essentially the soil that Marxian Economics was grown in. Children were working 16 hours a day, robbed of their childhood. Women were paid dirt and made to work in dangerous conditions. Sewage ran in the streets and the rivers - cholera spiked. The sky was black from coal dust and smoke. Worker accidents were prevalent with many workers dying. Healthcare was unheard of. Supply chains were exploitative at the highest level (they were empire, not business). And now, subsistence farming was beginning to be impossible - people were forced to urbanize and work in these conditions. It was truly horrible.

So, when contemplating ME, you must:

Keep the above in mind. If you disagree with the philosophy, you should at least understand what catalyzed its development.

Remember these conditions exist today. The cobalt in our phones, the textiles from Bangladesh. We cover up our exploitation with Amazon packaging and fruit logos.

Marxian Method

In my estimation, the most valuable knowledge from ME is Marxian Method. It provides a theoretical framework for creating theories of the world.

Before we begin, we need to provide some simple definitions:

Concrete: This term refers to objects, concepts, or ideas that are tangible, physical, and can be perceived directly through the senses. Concrete items are specific and have a physical presence that can be seen, touched, heard, smelled, or tasted.

Abstract: This term refers to ideas, concepts, or qualities that are intangible and cannot be perceived through the senses directly. Abstract concepts are often complex and can represent ideas, feelings, states, or qualities that do not have a physical presence. Examples of abstract concepts include love, justice, freedom, and mathematics. These are understood intellectually rather than through direct sensory experience.

The essence of Marxian Method is:

Concrete Observations

Observing Reality as it is.

Abstraction

The rational process in which the researcher looks for general characteristics that determine the concrete. This is essentially discerning principles that govern the behavior of the concrete.

Concrete Predictions

From this abstraction of principles you can create predictions of the behavior of the concrete.

Concrete Observations

From these predictions you see how accurate you were through observation.

Refine Abstraction

You refine your abstractions to get closer at truth.

This can be simplified to the following diagram:

This is only briefly touching upon Marxian Method which is deeply rooted in Hegelian Idealism and other philosophical concepts (link). The essence of the Marxian Method lies in this structured progression from concrete observations to refined abstractions based on those observations. It is a powerful method to use when approaching any domain.

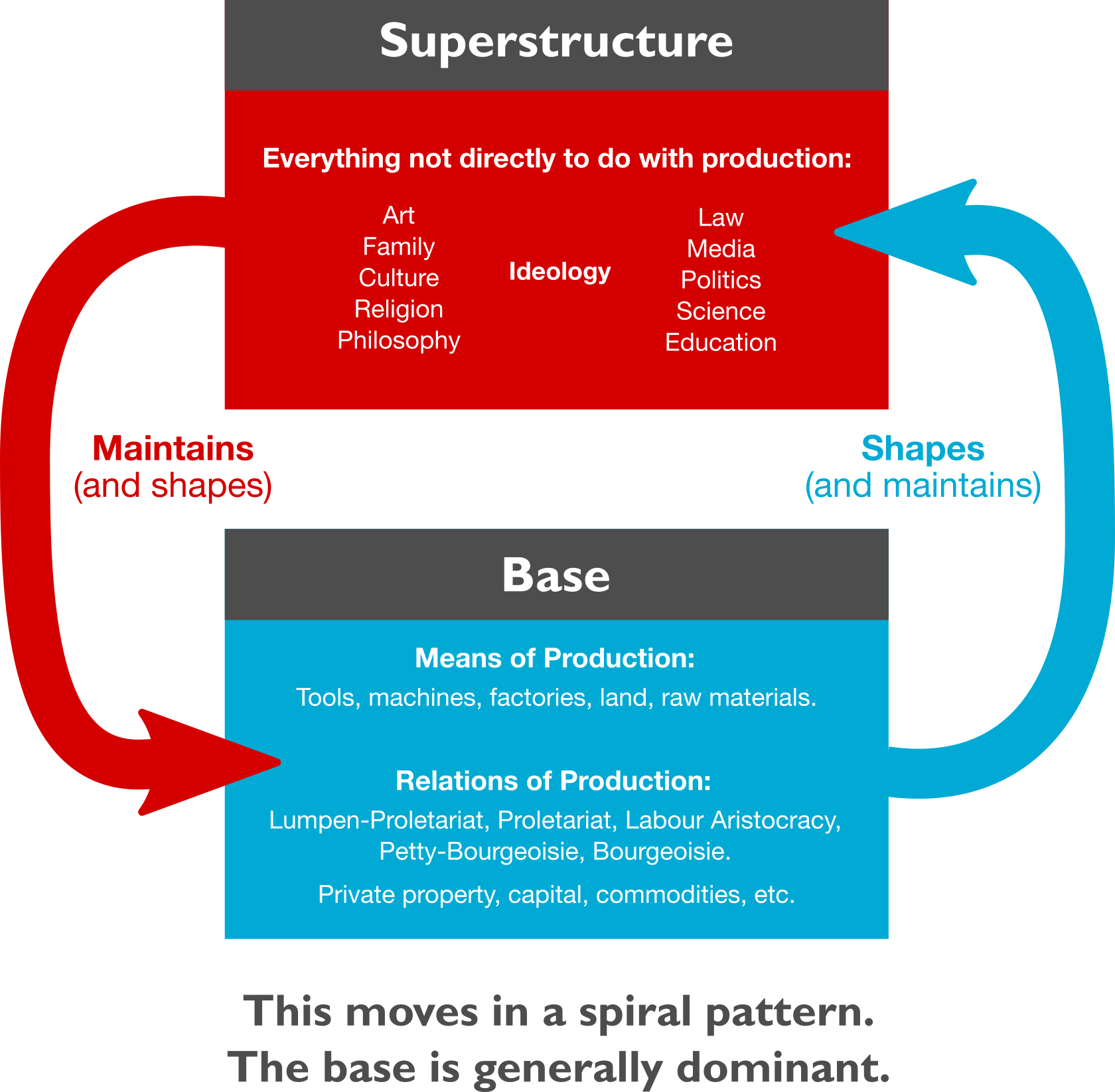

Base & Superstructure

One of the profound abstractions that came out of Marx’s work are the concepts of the Base and the Superstructure and how they interact with one another.

{kind=link}

The "base" refers to the mode of production in a society, encompassing the means of production (e.g., land, factories, technology, capital) and the relations of production (e.g., class relationships, labor arrangements). The economic base determines the social and political structures of a society by dictating what is produced, how it is produced, and who controls the means and results of production. According to Marx, the economic base is the foundation upon which all other aspects of society are built and is the primary force driving historical change.

The "superstructure" consists of the social, political, legal, cultural, and ideological systems and institutions that arise from and serve to maintain the economic base. This includes the state, legal systems, educational systems, family structures, media, and religious institutions. The superstructure is shaped by and reflects the interests of the ruling class that controls the economic base, reinforcing and legitimizing the existing class structure and relations of production.

Marx argued that while the economic base fundamentally shapes the superstructure, there is also a reciprocal relationship where the superstructure can influence and sustain the base. This interaction contributes to the stability of a given mode of production but also contains the seeds of social and political conflict, as changes in the economic base can lead to conflicts within the superstructure, ultimately driving societal transformation.

This is a powerful way for one to conceptualize the economy and gives a model to understand how technological innovation can change things such as culture, law, politics, etc. It has given me value in my investment due diligence when analyzing the potential disruption from an innovative new technology. One could use this model to assess the base & superstructure impact of Generative AI for instance.

Labor Theory of Value

This is where Marx and I significantly diverge.

The labor theory of value is a foundational concept positing that the value of a commodity can be objectively measured by the average number of labor hours required to produce it. According to this theory, the value of a product is determined not by the subjective utility it may provide to its consumer nor by the price it brings in the market, but by the total labor socially necessary for its production, including direct labor (actual manufacturing) and indirect labor (the production of tools, machines, etc., used in manufacturing). Marx used this theory to argue that all surplus value (profit) generated in a capitalist system derives from the exploitation of labor, as workers are paid less than the value of the goods they produce, with the difference being appropriated by capitalists as profit. This theory highlights the central role of labor in the creation of value and the inherent conflict between capital and labor under capitalism.

Marx is working upon a flawed axiom. To me, clearly, value is an emergent property resulting from the entire set of inputs put together in a way that is fit order and matches the needs of the environment (in this case the market). Value emerges from all elements and the structured fitness of the creation — that determines value — which is then assigned a numerical value by the market.

Additionally, not all labor can be held equal in the creation of value. I would assign greater value attribution to the entrepreneur, director, or engineers of an organization. To what degree and to what amount I have no idea — but certainly not the discrepancy we are seeing today (CEO pay has skyrocketed 1,460% since 1978). In the future I would like to see a more objective financial framework for executive compensation that maybe emerges from ESG or some other framework.

Strict ideological adherence to the labor theory of value can result in serious pathology. If “labor” feels that they are the sole source of value, then they are willing to tear down the institutions and directors that in their assessment clearly have no value.

A stark illustration of the consequences of misapplying economic theories can be seen in the tragic outcomes in both the Soviet Union and Zimbabwe, where the mass killing or expropriation of farmers' land led to widespread famine. This stems from the flawed notion that all types of labor contribute equally to value creation, thereby underestimating the unique and crucial contributions of certain “classes”. Such oversimplifications can devalue the essential roles certain groups play, setting the stage for catastrophic decisions that can devastate societies.

Historical examples where policies based on simplified or dogmatic interpretations of economic theories have led to catastrophic results. These negative results highlight the need for economic models that reflect the complexity of real-world economies and the diverse contributions to value creation.

Alienation of Labor

Alienation of labor is a concept highlighting a fundamental disconnect and estrangement workers feel from the products of their labor, the labor process, themselves, and their fellow workers within the capitalist system. Marx posited that in capitalism, workers do not own what they produce; instead, their labor becomes a commodity, and the products of their labor are taken away and sold by capitalists for profit. This process dehumanizes workers, reducing their creative and productive activity to mere means of survival, and strips them of the ability to assert control over their work and its outcomes. Consequently, workers become alienated not only from the fruits of their labor but also from their innate potential for creativity and community, leading to a sense of isolation and dissatisfaction that pervades their work and life.

Why am I mentioning the alienation of labor? Artificial Intelligence.

AI is setting the stage to completely disrupt or possibly upheave the labor market. This could result in a positive outcome or a negative outcome — but most likely both. The cliche “idle hands are the devil’s workshop” holds some explanatory utility here - as mass unemployment could cause social dishevelment, friction, or conflict. Even today they homesteading and craft revival movements are a direct result from alienation of labor.

Marxian Economics Conclusion

Exploring Marxian economics offers valuable insights, given its wide-reaching impact it is essential for understanding both the 20th century and our current era. Regardless of whether one agrees or disagrees with its principles, grasping Marxian economics is crucial for comprehending the historical and socio-economic developments that have shaped the modern world today.

However, a word of caution. Don’t get swept away in the romance of the proletariat. Especially until you have hired some.

Remember, the road to hell is paved in good intentions.

Don’t tear down your own house.

However, at the same time, also don’t be one of these foolish people who sticks their head in the sand and hums a Disney tune while ignoring the broad based economic slavery proliferating today. We can work together in a moderate and wise way to make our world better.

Marxian Post Script:

I always found it funny that Marx wrote Das Kapital with his time off paid for by the capitalistic profits of a rich friend’s textile mills (Friedrich Engels). Therefore, in a way, this demonstrates capitalisms self-destructive process Marx discusses.

Anyway, Marx’s book was paid for by the exploitation of labor by his buddy Engel’s textile factories. It was very entrepreneurial of him to understand that the exploitation of labor should fund his book.

Limits, Errors, Omissions, Gaps, & Lags

Now we are going to talk about the limits of the science of economics. Specifically, we will be looking at the process from which you go from defining a set to reaching “knowledge”, a conclusion, a decision, and/or an action. This section all comes down to exploring and questioning the relative reliability of economics for knowledge generation and decision making.

Defining a Set

Before collecting any data, you must first define the scope (i.e. set), of reality you will be isolating to collect your data within. This set can be a global economy, a national economy, a state or provincial economy, a municipality or township economy, a household, an industry, a market, a subsection or cross-section of any of the aforementioned, even yourself as an individual (though we typically just call this accounting). The total number of potential sets are infinite (however the total number of potential useful sets is most likely less than infinite).

Sets typically should be defined by ontological reality or utility, one of the two. If defined by ontological reality, I recommend they be defined by emergence (a later blog post will explain this method), if defined by utility, they are completely arbitrary and should be defined by use-value.

In the context of economics, "ontological reality" refers to the essential and inherent characteristics of a phenomenon as it exists independently of any conceptualization or interpretation. This term is used to identify and define economic sets based on their real, objective existence rather than their perceived usefulness or practical application. When a set is defined by ontological reality in economics, it implies that the set includes elements that are fundamentally part of the economic system under consideration, such as the inherent properties and behaviors of a market or economy. This approach to defining sets focuses on understanding the intrinsic nature of economic phenomena to ensure that data collection and analysis are grounded in the actual structures and dynamics of the economy, rather than being shaped by subjective or arbitrary criteria.

Defining any ontological reality is a very difficult game to play as the world is infinitely connected. There are almost no sets existing in actuality/reality outside the human mind. So describing reality as a system of sets is an inaccurate though useful way to go about orienting ourselves within reality. To a large degree industries and markets are arbitrary sets and you can draw their boundaries based on need. But these lines don't exist in reality - per se.

Defining a set by utility involves selecting a scope of study based on its practical value or relevance to specific objectives. This approach is essentially pragmatic, focusing on how useful the data collected within this set will be for achieving desired outcomes, such as understanding market trends, forecasting economic conditions, or informing policy decisions.

When sets are defined by utility, the boundaries are drawn not based on inherent characteristics of the economic phenomena but rather on the needs and goals of the research or analysis being conducted. For example, a researcher might define a market set that includes only certain types of consumers or transactions that are relevant to a specific question or hypothesis. Similarly, a policy analyst might focus on a subset of economic activities that are directly impacted by a proposed regulation.

This method of set definition allows for flexibility and adaptability, enabling analysts and researchers to tailor their investigations to suit particular interests or requirements. However, it also means that the defined sets may not fully represent the complete, objective nature of the economic systems they study, as they are constructed specifically to serve a particular purpose or to address specific questions.

Visualizing This Process

Below are some illustrations from Brian Greene explaining the concept of SpaceTime. Though this is from the field of physics, it is a useful analogy for the definition and assumption of sets.

When looking at the images below:

Assume the loaf of bread is the set of economic totality (all economic reality).

Assume the highlighted sections (in yellow and red) are the sets you are defining, assuming, and “pulling out” of reality.

You can establish categories to look at reality in a way (any way) from your perspective that is relevant to your perspective, objective, or “now”. All are valid perspectives, they are just used in different ways to come to different conclusions based on need or even the experience and familiarity of the researcher.

Creativity in research, product development, or even art, has to do with the cross-referencing and connecting of disparate sets. Understanding this process of defining, cross-referencing, and utilizing sets can increase your creative power and effectiveness in all areas of life. Meaning, this is how you can cross reference the different areas of the loaf of bread to establish new categories, new concepts, new ideas, new creations.

A set, in a way, is defined from (by) a perspective. But it also aids in forming the perspective and for our purposes here, it represents the foundation of any analysis.

Collecting Data

Now you have your sets it is time to collect your data.

This process can be done through direct observation or through the collection of existing data (which is a second hand observation). This involves gathering the necessary information that reflects the dynamics within your defined set. There are two main approaches to data collection in economics:

Primary Data Collection: This method involves gathering new data that has not been previously collected. Techniques include surveys, interviews, experiments, and direct observation. Primary data is crucial when specific, up-to-date information is required, and when existing data sources do not meet the needs of your research. For instance, if you're studying the impact of a new policy on local businesses, conducting surveys to gather firsthand responses from business owners would be a primary data collection method.

Secondary Data Collection: This involves using data that has already been collected by others. Common sources include government publications, industry reports, historical data archives, and previous research studies. Secondary data is particularly useful for longitudinal studies where trends over time are analyzed, or when conducting preliminary analyses to identify patterns that may require more detailed investigation through primary data methods.

Challenges in Data Collection

While collecting data, you often face several challenges:

Availability: Sometimes the data needed might not be readily available, may be data from private institutions, or it may be cost-prohibitive to obtain.

Relevance: The available data might not perfectly align with the parameters of your defined set, leading to compromises in the scope of your analysis.

Quality: Data quality can vary significantly, with issues such as inaccuracies, lagging indicators, delays, missing data points, or biases, which can affect the reliability of your analysis.

Overcoming Challenges

To effectively handle these challenges, consider the following strategies:

Leverage Multiple Sources: Combining different data sources can compensate for the limitations of a single source and provide a more comprehensive view of the economic phenomena under study.

Data Cleaning and Validation: Invest time in cleaning and validating your data to ensure accuracy. This includes handling missing values, correcting errors, and validating assumptions through additional sources.

Technology and Tools: Utilize advanced data collection tools and technologies such as online surveys, data scraping tools, and analytics platforms that can streamline the process and enhance the quality of the data collected.

Trusting Economic Data

Many people, and many smart people, take issue with the quality and reliability of the data we collect. I know many gold bugs and traditional investors who don’t trust our inflation numbers and consider them to be essentially “gerrymandered” inflation metrics, gauges, and indexes. We will not go into whether they are correct or incorrect here, but the fact remains that many people take issue with the reliability of the data we collect and this is not something we can simply ignore.

There are many factors that lead to this distrust, some legitimate, some not (in my assessment). Some legitimate factors include; lagging indicators, complexity, incomplete data, misleading data, politically censored data (such as other nations lying about their Balance of Payments numbers), or even just human error. The underlying reality here, is you can never fully trust any data - even the data you collect yourself as we are all subject to human error.

There are however, some steps we can take to increase the relative trust we have in our data.

Trusting the data you collect is pivotal. Here, you evaluate the reliability and validity of your data sources. This involves scrutinizing the methods used to collect the data, understanding the potential biases in data collection, and recognizing the limitations of your data set. Economic research requires a critical approach where you continually question the veracity of the data before drawing any conclusions.

Ensuring Data Trustworthiness

Source Credibility: Always consider the credibility of the source from which the data originates. Peer-reviewed sources, established research institutions, and government databases typically provide more reliable data (but not always).

Cross-Verification/Triangulation: Where possible, verify the data through multiple sources or empirical testing. This is crucial for secondary data where the original data collection methods may not be directly observable.

Statistical Validation: Employ statistical techniques to test the robustness of your data. Techniques such as regression analysis, hypothesis testing, and error checking can provide insights into the reliability of the data.

Once you have come to a certain probabilistic preponderance to suggest your data is reliable you then process and analyze it.

Data Processing, Analysis, & Interpretation

In data processing, analysis, & interpretation the term “garbage in garbage out” could not apply more, so the previous section really matters. In some ways, the data verification is harder than the actual analysis as we have centuries of reliable statistical techniques, modern computers, and sophisticated software to nearly guarantee reliable calculations.

With the data collected and its reliability assessed, the next step is to process and analyze this data to extract meaningful insights. This often involves statistical analysis, econometric modeling, and the use of software tools like R, Python, or specialized economic analysis software like STATA or EViews. The objective here is to translate raw data into usable information that can inform business strategies. economic theories, policy decisions, or just your life in general.

Processing

Data processing involves:

Cleaning, organizing, classifying, and transforming data.

Performing calculations.

Visualizing Data.

Organizing metadata documentation for future reference.

There are many different resources to learn about data processing so I will not speak further on it here.

One specific challenge Economists face is they often have to work with incomplete or imperfect data. Working with inaccurate or incomplete data can be done but poses problems. This can be done with data imputation, robustness checks, use of proxy variables, survey adjustments, statistical modeling and other techniques using probability, triangulation, big data and machine learning, and finally by acknowledging limitations. These topics are beyond this blog post's scope, but I mention them for the more studious reader to explore.

Analysis

Now you have the data ready, we begin the process of analysis by breaking the subject/phenomena/data down to build it back up.

Analysis refers to the process of examining and breaking down a complex entity or situation into its constituent parts in order to understand its components, relationships, and underlying patterns. It involves a systematic approach to study data, information, or phenomena to gain insights and draw conclusions. Analysis can be qualitative or quantitative, depending on the nature of the data and the goals of the investigation.

It is essentially a process to tease apart the complexity in a systematic step by step manner with the goal of attaining knowledge, understanding, and clarity. This process integrates a mix of cognitive awareness, empirical methods, systemic thinking and intuition. It's a balance of reason and intuition, theory and practice, and individual insight and collective wisdom.

It is said that to truly understand anything in The Universe, you have to walk a circle around it, you have to see it from at least 12 different perspectives. Perspectives are infinite, and therefore analysis can be infinite. This means you have to know what the most important perspectives are to address, and also when to quit looking at perspectives and draw a conclusion. To aid in this I will break down my favorite types of analysis:

Basic Analysis

Basic analysis is the process of beginning to familiarize yourself with something. This includes the definitions, the components, efforts in disambiguation, and learning what others have discovered. It is also helpful to try and write the subject in your own words.

Philosophical Analysis

Philosophical analysis constitutes breaking the subject down into its philosophical components. This is where you question definitions, question presumptions and propositions. This is where you did deeper into something. Some may get frustrated with this analysis because it is so difficult to reach a conclusion, but it does deepen understanding.

Quantitative Analysis

Quantitative analysis is working with data and trying to understand something by putting it into a formal system. Many phenomena in life are functions, and a function can then be mapped to see internal workings and relationships. This also includes statistics, probability, and more advanced methods.

Qualitative Analysis

Qualitative analysis refers to the examination of non-numerical data to understand underlying patterns, themes, concepts, or insights. It's primarily concerned with understanding the deeper meaning, context, subtext, or subjective experiences related to the data

Historical/Time Series Analysis

Historical analysis provides the researcher with some understanding of how we got to the reality we are examining today as well as what forces drive change within the domain and how the domain evolves.

Component Analysis

This refers to breaking down the components more to gain a better understanding of them.

Structural Analysis

This involves examining how components interact and combine within a system in the subject under study.

System Analysis

Systems analysis goes up a level of abstraction and includes studying the system within which the phenomena you are studying is embedded in. For example, if you were studying a bank, a system analysis may then lead you to studying the broader financial system (locally, regionally, or nationally) that it is embedded within.

Environmental Analysis

This analysis includes looking at how the item under study functions within its broader environment or ecosystem. Building upon our last example of finance, at this level of analysis we would be looking at answering “how does finance fit in society overall?”

Cosmic Analysis

This is quite an interpretive analysis and has to do with answering what is the ultimate purpose of the thing being studied? How does it contribute to evolution overall? For example, what is the purpose of finance? Inter-temporal monetary exchange is the typical answer. But when you dig deeper you can see finance is a system of energy exchange similar to the fungal networks of soil connecting all trees.

Counterfactual, Gap, Omission Analysis

This analysis simply means, looking at the data of everything that happened and identifying what didn’t happen. Where are the gaps, what is omitted, what do these gaps and omissions mean. Yuval Harrari has a maxim for analysis that “the exception proves the rules”. By understanding what didn’t happen you can gain more insight into what you are studying.

Pattern Recognition

What are the patterns in the data?

Correlation & Causation Analysis

This analysis helps you understand the functioning of the system. What happens when an input is changed. Regression is great for this.

Perspectival Analysis

One of the investors of Spanx (the footless pantyhose) was a man and he said ‘he just didn’t get it’. But he still took the product home and showed his daughter and wife who raved about it — encouraging him to invest. He made an insane return on an investment he otherwise would have turned down if he hadn’t sought the opinions of others. We don’t know what biases we have, this is why having a diversity of perspectives is so key.

Altered Consciousness Analysis

Over the years many people have found it useful to contemplate something while under the influence of some substance.

Intuitive Analysis

Once you have reached a critical mass of understanding of a domain then your subconscious will start integrating massive amounts of data in a way you don’t even notice. At that point you can begin to ask yourself what you intuitively feel about domains.

Subtlety Analysis

What are the subtleties in the system? Are there small things that make a big difference?

Meta-Analysis

This analysis is one higher level of abstraction than all the others. When you go meta you jump from inside something to outside of it. This even includes analyzing how you are analyzing the subject.

Trends Analysis

This analysis includes looking over a shorter span of historical data and trying to identify trends, aka movements and momentums in certain directions.

Future Analysis

This analysis is simply, based on all the prior analyses (especially the trends), assessing how you think a domain or thing is going to evolve in the near future.

It's also worth noting that while the above analyses are presented in a format that implies sequential steps in practice, analysis can be iterative, dynamic, and constantly evolving. Through the process of analyzing something one might need to loop back to earlier steps based on new findings or insights. Additionally, in almost all instances of analysis, one will need to utilize "black boxes" until the cost-benefit of finding out what's in the black box is relevant. This means, that at many times throughout a process, educated guesses are required to move forward.

Interpretation

Interpretation refers to the process of explaining, understanding, or giving meaning to something. It involves making sense of information, data, events, texts, or experiences based on context, prior knowledge, and analytical skills. It is essentially the process of developing a conclusion, opinion, judgment, etc. through some process. It first involves synthesizing (bringing together) all that you’ve analyzed and then deciding what it means. Interpretation is also tricky, and therefore it becomes sort of an art.

Here are some reminders:

Remember, paradox is a core feature of reality. In some cases, there are some things that reason doesn’t explain (such as existence itself). Much of quantum physics is paradoxical and I wouldn’t be surprised if much advanced level economic phenomena is as well.

The menu is not the meal. The sign is not the way.

This phrase highlights the distinction between representations or descriptions of reality and reality itself. In the context of economics, this concept can be applied in several ways such as:

Economic Models vs Economic Reality: Economists often use models to represent complex economic systems. These models include assumptions and simplifications to make them workable. For example, the IS-LM model simplifies the relationships between interest rates and real output. Actual economies are far more complex, with countless variables interacting in unpredictable ways. No model can capture all the nuances of a real-world economy. The model might indicate certain outcomes, but these outcomes can differ in practice due to unforeseen factors.

Statistics vs Economic Reality: Economic indicators like GDP, unemployment rates, and inflation figures provide snapshots of economic health. These numbers are crucial for analysis and decision-making. The lived experiences of individuals and businesses can differ significantly from what the statistics suggest. For instance, a country may have a low unemployment rate, but this number might not reflect underemployment, job quality, or regional disparities.

Theoretical Assumptions vs Practical Applications: Many economic theories are built on assumptions such as rational behavior, perfect information, or efficient markets. These assumptions help in constructing theories and models. In the real world, human behavior often deviates from rationality, information is incomplete or asymmetric, and markets can be inefficient. Policies based solely on theoretical assumptions may fail if they do not account for these practical deviations.

Strangeloops:

A strangeloop describes a paradoxical structure that arises when, by moving upwards or downwards through a hierarchical system, one finds oneself back where one started. Strangeloops exist because of a self-reference problem. We ourselves are part of the truth we are trying to describe, which creates a strangeloop problem. The finger cannot point at itself. But we can understand reality to a certain degree, but it requires a radically new state of consciousness, an epiphany. Remember that the economy is full of strangeloops.

When in doubt use a series of educated guesses and keep testing empirically.

There are endless amounts of ways to interpret the world and that disorients the human in terms of knowing what they should do. But that doesn’t mean there are endless amounts of productive, meaningful, and sustainable ways to interpret the world. The hallmarks of a good interpretation are description, prediction, and usefulness. In addition to all the above challenges, economic conclusions are very valuable to political debates so the words of economists will inevitably be twisted by those who wish to use them. So even if you discover something real and true, be prepared for it to be ‘twisted by knaves and fools’.

Limits, Errors, Omissions, Gaps, & Lags: Conclusion

The whole purpose of this section was to express that it is important to approach the field of economics with humility (as well as giving an overview of how to draw conclusions from economic data).

Navigating the complex terrain of economic data collection, processing, analysis, and interpretation is both a challenging and enlightening endeavor. The journey from defining a set to drawing conclusions involves rigorous steps that help mitigate the inherent limits, errors, omissions, gaps, and lags in economic research. By understanding the necessity of clearly defining the scope of study, whether through ontological reality or utility, and by employing meticulous data collection and validation techniques, we can improve the reliability of our analyses.

However, it is crucial to acknowledge that no data set is perfect and no analysis is infallible. The field of economics is fraught with uncertainties, and even the most sophisticated models and methods cannot completely eliminate the risk of error. This inherent uncertainty underscores the importance of humility in economic research. Recognizing the limitations of our knowledge can prevent the overconfidence that often leads to misguided policies and decisions with far-reaching negative consequences.

The illusion of complete knowledge in economics can be particularly dangerous. By maintaining a critical and humble approach, continuously questioning the data, and being open to multiple perspectives and interpretations, we can better navigate the complexities of economic phenomena. The systematic approach outlined in this section provides a framework for drawing more reliable and meaningful conclusions, but it is essential to remain vigilant and adaptable to the ever-changing dynamics of economic systems.

In essence, the process of drawing economic conclusions is indeed dark and full of terrors, but it is also a path to greater understanding and insight. By embracing the uncertainties and complexities of the field, we can contribute to a more robust and nuanced understanding of economic realities, ultimately fostering more informed and effective decision-making.

The Next Evolution of Economics - Where I See It Going

Economics is an evolving field, it is never static. Rather, it is a dynamic field of study influenced by a myriad of factors. Economics, as a field itself, is also a complex adaptive system (similar to the economy). The field itself will evolve in predictable and unpredictable ways. Here are some of my ideas on where I see the field going.

It will broaden its purpose:

Have you ever thought why we study economics?

The traditional answer to this question has included the following:

Understanding human economic behavior.

Understanding resource allocation.

Understanding decision making.

Understanding markets.

Informing business decisions.

Informing public policy.

Encouraging economic growth and development.

Addressing societal needs.

I believe these reasons are still somewhat shortsighted. To me, the primary purpose of economics is to understand how humans survive, how humans thrive, and to aid in helping humans thrive.

The world used to be a very scarce place, so the field of Economic’s primary focus on production throughout history was necessary and natural. However, as we move closer to production and distribution of products and services being optimized, I think the core intentions and focus of economics will evolve as well. I believe the focus will evolve from production and distribution, to human wellness, to human fulfillment, and eventually to human self-actualization. Economics, in its essence is about how humans survive in their environment. It is a natural extension to now ask the question how do we use our resources to help humankind thrive.

GDP, GNP, and other economic measurements, though useful, highlight the wrong aspects of “progress”. Growth is not everything, biodiversity is an asset, and we need clean air, clean land, and clean water to continue our life as a species on this Earth. Only recently have we been measuring the depletion of Earth’s balance sheet through economic activity. This suggests a fundamental flaw in our practice of capitalism: if our most fundamental balance sheet (Earth) is depleting, then our economic activities are not truly profitable. If our liabilities outweigh our assets, then we are in a vortex of diminishing returns.

From broadening our conceptualization of the purpose and intention of economics new questions will emerge. A job, a purpose, and happiness are intimately connected. As we use the field of economics to discover ways to be more effective in our economic activities, we can begin to make jobs safer, more fulfilling, and discover how we can go about using economic knowledge to help people live a fulfilling life and create a coalition of sentient beings.

It is important to note that this new intention, builds upon the old focus of production. It does not replace it. Without production we do not have the ability to focus on the questions of how we as a species can thrive. This new intention evolves from the old focus and instead asks what is next, how can we improve further.

It will broaden its scope:

From this new purpose/intention the field of economics will have to broaden its scope. Simply put, the field of economics will have to be more inclusive of beliefs/perspectives, behaviors, people, and work in other fields. The field should trend to encompassing everything that makes human's thrive. Let’s start with some non-radical observations

Housework must be measured and given an economic value. This clearly has economic value even though it is not measured in GDP. Without this measurement we haven’t been able to see the economic loss of two parent households. It is not just a full economic gain to GDP, the household loses that productivity and that loss manifests in other ways not seen until children are adults.

If production is the only thing measured, but everyone is miserable, and suicide rates are going up (which they are), then what is the purpose of the production in the first place? Ways to measure health, wellness, and fulfillment need to be borrowed from psychology, sociology, and other fields. There are ways to turn these abstract concepts to models and measurable phenomenon. For example, a drop in suicide rates can be measured, a drop in hypertension can be measured, etc. Over time new models that measure these abstract concepts can be refined and new metrics can be envisioned within indexes.

Economics is fundamentally about how humans survive. The field will become more robust from the contributions of all other scientists, sciences, and technologies.

George Soros was famous for saying that the prevailing paradigm influences reality, which then changes the paradigm. Economic research in wellness, fulfillment, and actualization will help redirect resources to go away from conspicuous and compulsive consumption (or maybe this is wishful thinking, but I will choose hope on this one).

Simply put, broadening the scope of economics is including economically valuable behaviors, different perspectives, and more of the work in other fields.

New technology & techniques:

Recent innovations in technology and techniques are poised to significantly impact the way economic analysis, research, and its resulting business and policy-making are conducted. Here are some key innovations that could have a massive impact on the field:

Big Data and Advanced Data Analytics

Enhanced Data Collection: The availability of large datasets from diverse sources, such as social media, transaction records, and IoT devices, allows economists to analyze economic behaviors and trends with greater precision.

Real-Time Data: IoT devices provide real-time data on economic activities, such as production processes, consumption patterns, and logistics, enabling more responsive and informed economic decisions.

Satellite Data: Satellite data can monitor environmental changes, land use, and natural resource management, providing valuable information for environmental and resource economics.

Advanced Analytics: Machine learning and artificial intelligence (AI) techniques are used to analyze complex datasets, uncover patterns, and make predictions about economic phenomena. There are also new possibilities in dark data (data that is collected but not used) and digital twins (a virtual representation of a physical object, system, or process that mirrors its real-world counterpart in real time) that could revolutionize our accuracy and effectiveness.

AI and ML

Predictive Modeling: AI and machine learning models can improve the accuracy of economic forecasts by analyzing vast amounts of data and identifying underlying trends.

Automated Decision Making: AI-driven algorithms can assist in making real-time economic decisions, such as in financial markets or policy implementations.

LLMs